Overview

SelectBoost.quantile adapts the SelectBoost idea to

sparse quantile regression. A typical workflow is:

- fit a quantile model with

selectboost_quantile(), - inspect the selection-frequency path,

- extract a stable support with

summary()orsupport_selectboost_quantile(), - optionally tune the penalty explicitly with

tune_lambda_quantile().

The current package defaults are designed to be reasonably

conservative: screening is activated automatically in

p > n settings, tuning can use a 1-SE rule with penalty

inflation, and stable support extraction defaults to a hybrid score that

combines path stability and fitted effect size.

Simulate a correlated design

load_selectboost_quantile <- function() {

if (requireNamespace("SelectBoost.quantile", quietly = TRUE)) {

library(SelectBoost.quantile)

return(invisible(TRUE))

}

if (!requireNamespace("pkgload", quietly = TRUE)) {

stop(

"SelectBoost.quantile is not installed and pkgload is unavailable.",

call. = FALSE

)

}

roots <- c(".", "..")

roots <- roots[file.exists(file.path(roots, "DESCRIPTION"))]

if (!length(roots)) {

stop("Could not locate the package root for SelectBoost.quantile.", call. = FALSE)

}

pkgload::load_all(roots[[1]], export_all = FALSE, helpers = FALSE, quiet = TRUE)

invisible(TRUE)

}

load_selectboost_quantile()

sim <- simulate_quantile_data(

n = 100,

p = 20,

active = 1:4,

rho = 0.7,

correlation = "toeplitz",

tau = 0.5,

seed = 1

)Fit a first model

fit <- selectboost_quantile(

sim$x,

sim$y,

tau = 0.5,

B = 6,

step_num = 0.5,

screen = "auto",

tune_lambda = "cv",

lambda_rule = "one_se",

lambda_inflation = 1.25,

subsamples = 4,

sample_fraction = 0.5,

complementary_pairs = TRUE,

max_group_size = 10,

seed = 1,

verbose = FALSE

)

print(fit)

#> SelectBoost-style quantile regression sketch

#> tau: 0.5

#> perturbation replicates: 6

#> c0 thresholds: 5

#> predictors: 20

#> grouping: group_neighbors

#> max group size: 10

#> screening: none

#> stability selection: 4 draws at fraction 0.5 (complementary pairs)

#> tuned lambda factor: 0.7789 (cv, one_se)

#> top mean selection frequencies:

#> x2 x1 x3 x4 x17 x5

#> 0.883 0.875 0.771 0.688 0.583 0.579The printed object summarizes the perturbation path, tuning choice, screening rule, and the highest mean selection frequencies.

Summarize and extract stable support

smry <- summary(fit)

smry

#> Tau: 0.5

#> Stable support threshold: 0.55

#> Selection metric: hybrid

#> Variables above the threshold:

#> [1] "x2" "x1" "x3"

#> Top summary scores:

#> x2 x1 x3 x4 x13 x17 x5 x14 x12 x10

#> 0.871 0.863 0.686 0.513 0.189 0.164 0.080 0.069 0.044 0.022

support_selectboost_quantile(fit)

#> [1] "x2" "x1" "x3"

coef(fit, threshold = 0.55)

#> (Intercept) x1 x2 x3 x4

#> -2.892020e-01 1.910100e+00 1.653308e+00 -9.918470e-01 6.193026e-01

#> x5 x7 x11 x14 x17

#> 4.772659e-02 -6.892092e-12 6.177269e-11 -6.625734e-02 8.629423e-02

#> x18 x19 x20

#> 4.285874e-12 1.149629e-11 2.044608e-11By default, summary() and

support_selectboost_quantile() use the hybrid support

score. If you want the older frequency-only rule, use

selection_metric = "frequency".

support_selectboost_quantile(

fit,

threshold = 0.55,

selection_metric = "frequency"

)

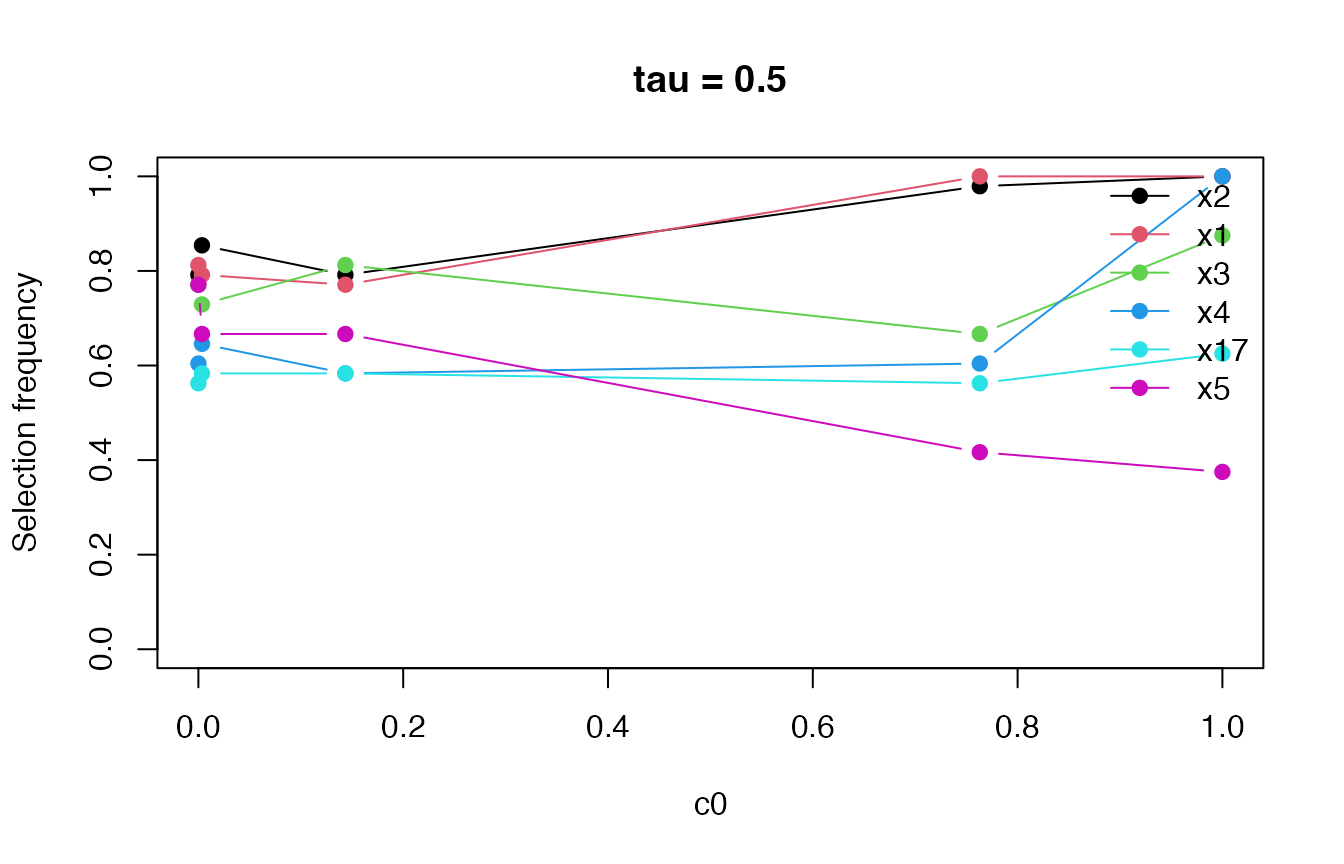

#> [1] "x1" "x2" "x3" "x4" "x5" "x7" "x11" "x14" "x17" "x18" "x19" "x20"Plot the frequency path

plot(fit)

The path can help distinguish variables that remain stable under stronger perturbations from variables that are selected only when the perturbation is weak.

Formula interface and multiple quantiles

dat <- data.frame(y = sim$y, sim$x)

fit_formula <- selectboost_quantile(

y ~ .,

data = dat,

tau = c(0.25, 0.5, 0.75),

B = 4,

step_num = 0.5,

tune_lambda = "bic",

seed = 2,

verbose = FALSE

)

print(fit_formula)

#> SelectBoost-style quantile regression sketch

#> tau: 0.25, 0.50, 0.75

#> perturbation replicates: 4

#> c0 thresholds: 5

#> predictors: 20

#> grouping: group_neighbors

#> screening: none

#> tuned lambda factors: 1.0000, 0.5322, 1.0000

#> tau = 0.25: top mean selection frequencies

#> x1 x2 x3 x20

#> 0.95 0.85 0.85 0.85

#> tau = 0.5: top mean selection frequencies

#> x17 x3 x4 x5

#> 0.95 0.90 0.90 0.90

#> tau = 0.75: top mean selection frequencies

#> x1 x3 x4 x16

#> 0.85 0.80 0.80 0.80

summary(fit_formula, tau = 0.5)

#> Tau: 0.5

#> Stable support threshold: 0.55

#> Selection metric: hybrid

#> Variables above the threshold:

#> [1] "x2" "x3" "x1"

#> Top summary scores:

#> x2 x3 x1 x4 x17 x5 x13 x14 x12 x6

#> 0.850 0.832 0.750 0.502 0.300 0.265 0.222 0.185 0.178 0.000Predictions can be extracted from either matrix- or formula-based fits.

predict(

fit_formula,

newdata = dat[1:3, -1, drop = FALSE],

tau = 0.5

)

#> 1 2 3

#> -1.7911186 0.2847084 -2.5857687Inspect penalty tuning directly

tuned <- tune_lambda_quantile(

sim$x,

sim$y,

tau = 0.5,

method = "cv",

rule = "one_se",

lambda_inflation = 1.25,

nlambda = 6,

folds = 3,

repeats = 2,

seed = 3,

verbose = FALSE

)

print(tuned)

#> Quantile-lasso tuning

#> tau: 0.5

#> method: cv

#> rule: one_se

#> lambda inflation: 1.25

#> folds: 3

#> repeats: 2

#> selected factor: 0.6866

#> score: 0.49975

#> standard error: 0.012345

summary(tuned)

#> tau factor score se rule lambda_inflation selected

#> 1 0.5 1.00000000 0.5243058 0.0007634017 one_se 1.25 FALSE

#> 2 0.5 0.54928027 0.4997532 0.0123450390 one_se 1.25 TRUE

#> 3 0.5 0.30170882 0.5193880 0.0048581777 one_se 1.25 FALSE

#> 4 0.5 0.16572270 0.5402414 0.0016910207 one_se 1.25 FALSE

#> 5 0.5 0.09102821 0.5487809 0.0123171347 one_se 1.25 FALSE

#> 6 0.5 0.05000000 0.5514630 0.0199834361 one_se 1.25 FALSENext steps

- Use

vignette("validation-study", package = "SelectBoost.quantile")to see how the current selector compares with the lasso baselines on the shipped benchmark study. - Use

benchmark_quantile_selection()if you want to evaluate the method on a different simulation grid.