Frédéric Bertrand

SelectBoost.quantile adapts the SelectBoost idea to sparse quantile regression. The package builds correlation neighborhoods, perturbs correlated predictors with a directional sampler inspired by the original SelectBoost internals, refits penalized quantile regression models on the perturbed designs, and aggregates variable-selection frequencies across a path of correlation thresholds.

The current package already supports:

- matrix and formula interfaces,

- single- and multi-

tauworkflows, - tau-aware screening for

p > nsettings, - stronger penalty tuning through one-standard-error selection and lambda inflation,

- complementary-pairs stability selection,

- neighborhood capping for high-dimensional correlated designs,

- hybrid support extraction that combines path stability and fitted effect size,

- benchmark helpers for validation studies.

The package should still be read as a methodological prototype: the workflow is usable and documented, but the quantile-regression adaptation is still being validated and refined.

Start with vignette("getting-started", package = "SelectBoost.quantile") for the main workflow, then use vignette("validation-study", package = "SelectBoost.quantile") for the shipped benchmark comparisons.

Installation

You can install the development version of SelectBoost.quantile from GitHub with:

remotes::install_github("fbertran/SelectBoost.quantile")From a local source checkout, use:

devtools::install()Main workflow

For each correlation threshold c0, selectboost_quantile():

- normalizes the design as in the original

SelectBoostworkflow, - builds correlation neighborhoods,

- fits a sign-aligned directional model to each neighborhood,

- perturbs the predictors in the sample hyperplane,

- refits sparse quantile regression,

- aggregates the selection frequencies across perturbations and stability subsamples.

The resulting frequency path can then be summarized, plotted, or thresholded into a stable support.

Example: matrix interface

library(SelectBoost.quantile)

sim <- simulate_quantile_data(

n = 100,

p = 20,

active = 1:4,

rho = 0.7,

seed = 1

)

fit <- selectboost_quantile(

sim$x,

sim$y,

tau = 0.5,

B = 6,

step_num = 0.5,

screen = "auto",

tune_lambda = "cv",

lambda_rule = "one_se",

lambda_inflation = 1.25,

subsamples = 4,

sample_fraction = 0.5,

complementary_pairs = TRUE,

max_group_size = 10,

seed = 1,

verbose = FALSE

)

print(fit)

#> SelectBoost-style quantile regression sketch

#> tau: 0.5

#> perturbation replicates: 6

#> c0 thresholds: 5

#> predictors: 20

#> grouping: group_neighbors

#> max group size: 10

#> screening: none

#> stability selection: 4 draws at fraction 0.5 (complementary pairs)

#> tuned lambda factor: 0.7789 (cv, one_se)

#> top mean selection frequencies:

#> x2 x1 x3 x4 x17 x5

#> 0.883 0.875 0.771 0.688 0.583 0.579

summary(fit)

#> Tau: 0.5

#> Stable support threshold: 0.55

#> Selection metric: hybrid

#> Variables above the threshold:

#> [1] "x2" "x1" "x3"

#> Top summary scores:

#> x2 x1 x3 x4 x13 x17 x5 x14 x12 x10

#> 0.871 0.863 0.686 0.513 0.189 0.164 0.080 0.069 0.044 0.022

support_selectboost_quantile(fit)

#> [1] "x2" "x1" "x3"

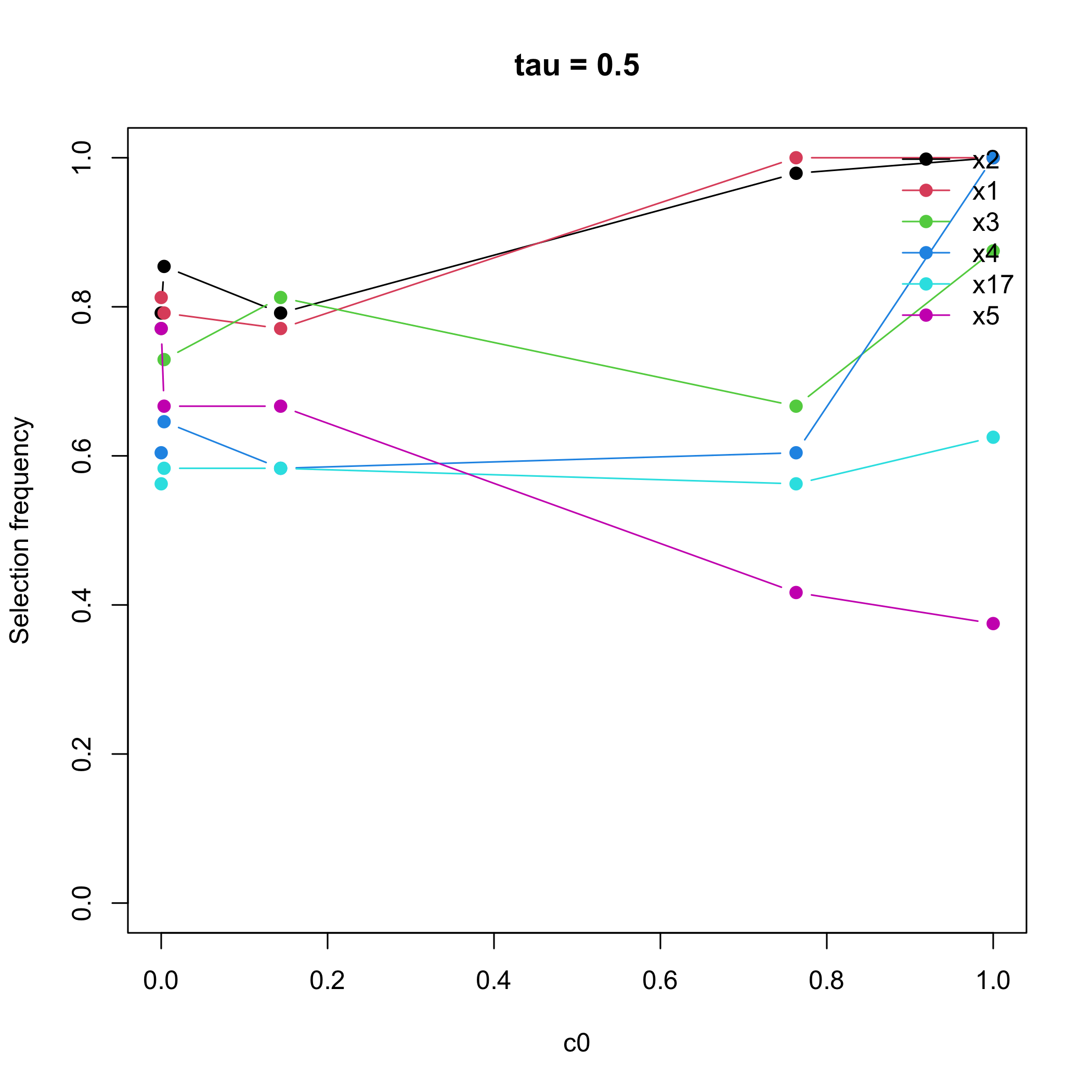

plot(fit)

Selection-frequency paths for the six variables with the highest mean selection frequency.

Example: formula interface and multiple quantiles

dat <- data.frame(y = sim$y, sim$x)

fit_formula <- selectboost_quantile(

y ~ .,

data = dat,

tau = c(0.25, 0.5, 0.75),

B = 4,

step_num = 0.5,

tune_lambda = "bic",

seed = 2,

verbose = FALSE

)

print(fit_formula)

#> SelectBoost-style quantile regression sketch

#> tau: 0.25, 0.50, 0.75

#> perturbation replicates: 4

#> c0 thresholds: 5

#> predictors: 20

#> grouping: group_neighbors

#> screening: none

#> tuned lambda factors: 1.0000, 0.5322, 1.0000

#> tau = 0.25: top mean selection frequencies

#> x1 x2 x3 x20

#> 0.95 0.85 0.85 0.85

#> tau = 0.5: top mean selection frequencies

#> x17 x3 x4 x5

#> 0.95 0.90 0.90 0.90

#> tau = 0.75: top mean selection frequencies

#> x1 x3 x4 x16

#> 0.85 0.80 0.80 0.80

summary(fit_formula)

#> SelectBoost quantile summary

#> tau values: 0.25, 0.50, 0.75

#> selection metric: hybrid

#> tau = 0.25: 3 variables above threshold

#> tau = 0.5: 3 variables above threshold

#> tau = 0.75: 4 variables above thresholdPenalty tuning

The package exposes the penalty-tuning stage directly through tune_lambda_quantile(). This is useful when the tuning decision itself needs to be inspected.

tuned <- tune_lambda_quantile(

sim$x,

sim$y,

tau = 0.5,

method = "cv",

rule = "one_se",

lambda_inflation = 1.25,

nlambda = 6,

folds = 3,

repeats = 2,

seed = 3,

verbose = FALSE

)

print(tuned)

#> Quantile-lasso tuning

#> tau: 0.5

#> method: cv

#> rule: one_se

#> lambda inflation: 1.25

#> folds: 3

#> repeats: 2

#> selected factor: 0.6866

#> score: 0.49975

#> standard error: 0.012345

summary(tuned)

#> tau factor score se rule lambda_inflation selected

#> 1 0.5 1.00000000 0.5243058 0.0007634017 one_se 1.25 FALSE

#> 2 0.5 0.54928027 0.4997532 0.0123450390 one_se 1.25 TRUE

#> 3 0.5 0.30170882 0.5193880 0.0048581777 one_se 1.25 FALSE

#> 4 0.5 0.16572270 0.5402414 0.0016910207 one_se 1.25 FALSE

#> 5 0.5 0.09102821 0.5487809 0.0123171347 one_se 1.25 FALSE

#> 6 0.5 0.05000000 0.5514630 0.0199834361 one_se 1.25 FALSEValidation workflow

The package includes a simulation and benchmark framework to compare plain quantile lasso, tuned quantile lasso, and the SelectBoost-based quantile workflow. The shipped validation study now reports recall, FDR, and F1 score.

scenarios <- default_quantile_benchmark_scenarios(

tau = c(0.25, 0.5),

regimes = c("moderate_corr", "high_dim")

)

bench <- benchmark_quantile_selection(

scenarios = scenarios,

replications = 5,

threshold = 0.55,

seed = 1,

verbose = TRUE

)

summary(bench)For a reproducible study from a source checkout, run:

out_dir <- file.path(tempdir(), "SelectBoost.quantile-validation")

system2(

"Rscript",

c("inst/scripts/run_quantile_benchmark.R", out_dir, "4", "0.55")

)The package ships both a getting-started vignette and a validation vignette: